Since 2018, restaurants had the luxury of deducting 100% of their build-out expenses and other fixed asset purchases, such as equipment and furniture, by claiming bonus depreciation on their tax returns. Starting in 2023, restaurants will no longer have this luxury. Bonus depreciation will be phased out over the next four years to 80% in 2023, 60% in 2024, 40% in 2025, and 20% in 2026.

Evolution of Bonus Depreciation

Bonus depreciation is a temporary tax benefit introduced in 2002 as part of the federal Job Creation and Worker Assistance Act. It allows businesses to accelerate depreciation tax deductions on their fixed asset purchases in the year placed in service, instead of having to depreciate the asset over its useful life slowly. The accelerated percentage has varied over the years from 30% to 100% (see Table 1 here), and it was at its most beneficial stage after the passing of the Tax Cuts and Jobs Act (TCJA) in 2017, when it increased to 100% and liberalized the qualifying assets. It expanded the qualification of assets to include used assets and qualified leasehold improvements, whereas historically, it only applied to new assets and personal property (vs. real property/build-outs/improvements/etc.).

Like interest rates, bonus depreciation has been used as an economic stimulation tool over the last twenty years to control US business investment and labor markets. It expired in 2007 due to increased spending, was reactivated in 2009 through 2012 due to the 2008 crash, and continues to be active today.

An Alternative to Bonus Depreciation

You might be wondering, if bonus depreciation was not always 100%, how did I write off 100% of my asset purchases in all those years? This brings us to another special business tax deduction widely used by restaurants– the Sec 179 deduction.

The Section 179 deduction allows businesses to deduct 100% of the purchase price of their qualifying fixed assets in the year placed in service up to a certain dollar limit. Unlike Bonus Depreciation, Section 179 is a permanent tax incentive dating back to 1958. It has an expensing limitation and a threshold for which the limitation begins to phase out. For 2023, the expense limitation is $1.16m. The 100% deduction begins to phase out on a dollar-for-dollar basis once your total fixed asset purchases for the year exceed $4.05m. The main differences between bonus depreciation and the sec 179 deduction are:

- The sec 179 deduction is limited to taxable income from all the taxpayer’s active trades or businesses. This means that the deduction flows through to the partner’s personal tax return, and if they don’t have any taxable business income to offset against the deduction, then it is unused in that year and carried forward to future years. On the other hand, bonus depreciation is allowed to generate a net operating loss (NOL) that can be applied toward other sources of income.

- Sec 179 can be applied on a property-by-property basis and for part of a property’s cost. Bonus depreciation automatically applies to all qualifying assets at their full costs minus any amounts expensed under Code Sec. 179. You can only opt out of bonus depreciation if you do it for all assets in the same class of asset (such as all equipment placed in service for that year). With bonus, you can’t pick and choose what you want to bonus.

As you can see, bonus depreciation is advantageous because it allows you to generate a net operating loss for your business, while sec 179 only allows you to zero out your business income. Sec 179 is advantageous because it provides more flexibility with how you pick and choose depreciation per asset.

The Impact of the NOL Limitation and Excess Business Loss Rules

Before 2021, taxpayers could offset their other sources of taxable income using business losses fully; any unused losses could be carried back or to future years to offset taxable income.Since sec 179 cannot generate an NOL, bonus depreciation was preferred. However, starting in 2021, After 2021, this is no longer the case. Business losses can only be claimed up to a certain amount each year, and NOLs are limited to 80% of taxable income when carried over. Therefore, generating an NOL using bonus depreciation is no longer attractive. We demonstrate this in the next section. In a separate article, we discuss the Excess Business Loss and NOL limitations.

Maximizing Depreciation Deductions in 2023 and Beyond

Now that you’re empowered with the fundamentals of bonus depreciation and sec 179 deduction, let’s demonstrate the optimal way to maximize tax savings given the post-2021 NOL limitation and bonus depreciation phase-out.

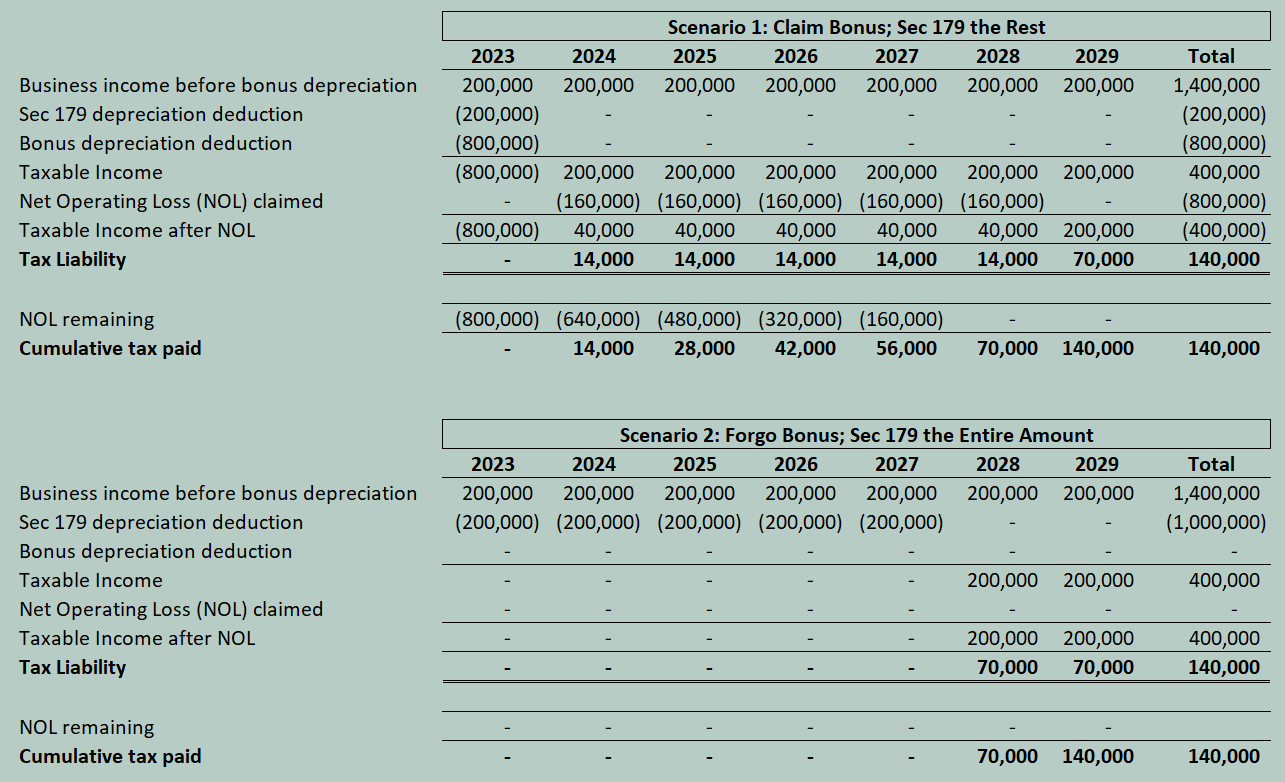

Assume a restaurant opens in 2023 with a $1m investment in build-out and equipment, and the restaurant generates $200k profit each year before considering depreciation. The forecast below demonstrates that claiming bonus depreciation in 2023 is not the best approach because although a huge NOL is created in the year placed in service, the NOL is not fully usable until 2029. Therefore, it’s more advantageous to opt out of the bonus and claim sec 179, which allows you to carry forward your sec 179 deduction and use 100% of it to offset business income for the first five years. Although the overall tax liability under both scenarios is the same, under Scenario 2, you are deferring tax payments to 2028.

This example assumes no standard/itemized deductions or credits, no other income sources that the NOL could offset, and that state tax implications are neutral. However, it’s enough to demonstrate how to strategically claim depreciation from 2023 onwards. Most states don’t recognize bonus depreciation or the sec 179 deduction; therefore, they must be added back to taxable income. However, some states allow for one but not the other up to a certain dollar amount. State tax implications must be considered when deciding how to depreciate assets.

Conclusion

Bonus depreciation is being phased out, and a new NOL limitation has arrived. You and your accountant must be wary of the implications and alternatives for claiming depreciation before doing what you have done in the past. Feel free to contact us to learn how you can strategically and proactively plan for taxes throughout the year via our monthly plans.