DC already has unfavorable taxes for restaurants – they charge a minimum gross receipts tax, don’t recognize pass-through entities for nonresident partners/shareholders, impose a sales tax on service charges, impose a high-income tax rate, and more. The DC minimum gross receipts tax (franchise tax) is imposed on your gross sales regardless of your profit. The fixed tax is $250 if your gross sales are under $1m and $1,000 if gross sales are over $1m. These taxes are annoying, but digestible. However, another tax based on gross receipts isn’t so digestible: the ballpark fee. Starting at $5,500/year, the ballpark fee now has a higher chance of applying to you due to Initiative 82. In this article, our restaurant CPA team will explain the ballpark fee return and how it could apply to more restaurants now that the tipped minimum wage is being phased out.

What is the DC ballpark fee?

The ballpark fee is collected from businesses with $5m or more in gross sales to cover the development, construction, and/or renovation costs of a ballpark in Washington, DC. The goal is to host professional athletic team events in DC.

Any business subject to filing franchise tax returns, such as the D-20 (corporation franchise tax) and D-30 (unincorporated business franchise tax), with over $5m in gross sales between June and May must file a Ballpark fee return through mytax.dc.gov by June 15 following the twelve months ending May 31. For example, the ballpark fee return due on June 15, 2024, should report the sales from June 1, 2023, through May 31, 2024.

It’s a very simple filing; you add your sales for the period, and mytax.dc.gov calculates the fee you owe.

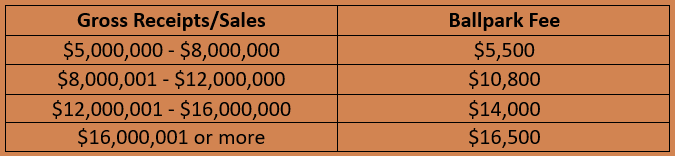

Here are the amounts you must pay based on your gross receipts/sales:

You still owe these fees even if you didn’t profit a single dime. More DC restaurants will find themselves subject to the ballpark fee due to rising prices and implementing service charges as a result of the tipped minimum wage phaseout.

These amounts are deposited into the Ballpark Revenue Fund. Each year before December 1, the DC Chief Financial Officer (CFO) assesses the revenue received in the prior year and expected revenue for the current year and determines whether the ballpark fee needs to increase for the upcoming year. Therefore, the fee is subject to change.

Multi-Unit Restaurant Groups and the Ballpark Fee

When a restaurant group parent company (holding company) wholly owns multiple LLCs (also known as single-member LLCs or disregarded entities because each LLC does not file a separate US federal tax return), it typically files a single DC tax return (Form D-20 or D-30). Each LLC has its mytax.dc.gov and sales tax accounts, but the ballpark fee is determined at the parent company level. For example, assume restaurants A, B, and C are separate LLCs owned 100% by Parent LLC, and each restaurant generates $2.5m in annual revenue. Parent LLC must file a ballpark fee return and pay $5,500 because its combined gross revenue exceeds $5m. Restaurants A, B, and C are not required to have ballpark fee accounts registered with DC, but Parent LLC is. The same principle applies if restaurants A, B, and C were not in separate LLCs and operated directly under Parent LLC.

Combined Reporting

When multiple bars or restaurants are engaged in a unitary business in DC, they must file a combined report when filing their annual form D-20 (corporate franchise tax return) or D-30 (unincorporated business tax return) instead of separate tax returns. This typically applies when you have a commonly owned or controlled group of restaurants, bars, commissaries, etc., that are sufficiently interdependent, integrated, and interrelated to provide mutual benefit. Click here to learn more about combined reporting in DC.

A unitary business is treated differently than a holding company for ballpark fee purposes. The ballpark fee is not determined and filed on a combined group basis. Each LLC or restaurant shall file and pay the ballpark fee if they individually meet the criteria for filing and paying the ballpark fee. For example, assume restaurants A, B, and C each generate $2.5m in annual revenue and file three separate federal income tax returns, but for DC purposes, they’re considered a unitary business and file a combined form D-30 (unincorporated business franchise tax return). Since they’re part of a combined report and the revenue is below $5m for each restaurant, none are subject to the ballpark fee.

Conclusion

The DC Ballpark fee and filing are relatively simple – especially compared to other taxes – but the nuances of exactly how the filing works for multi-unit restaurants and bars can be a little confusing. Whether your restaurant is a single unit, or has many storefronts, the advisors at the Fork CPAs can clarify any questions on the DC Ballpark fee, and have processes in place to make sure your filing is completed on time and you can view our restaurant accounting pricing to see how we can help. Schedule a call to get set up with a Fork CPAs engagement plan.